Key Takeaways

- Global energy investment reached a record USD 3.3 trillion in 2025, with clean energy attracting twice the capital of fossil fuels, while upstream oil investment fell for the first time since 2020.

- Oil and gas companies now run two portfolios inside one balance sheet: mature hydrocarbon assets that generate today's cash, and transition investments with different economics, risk profiles and capital cycles.

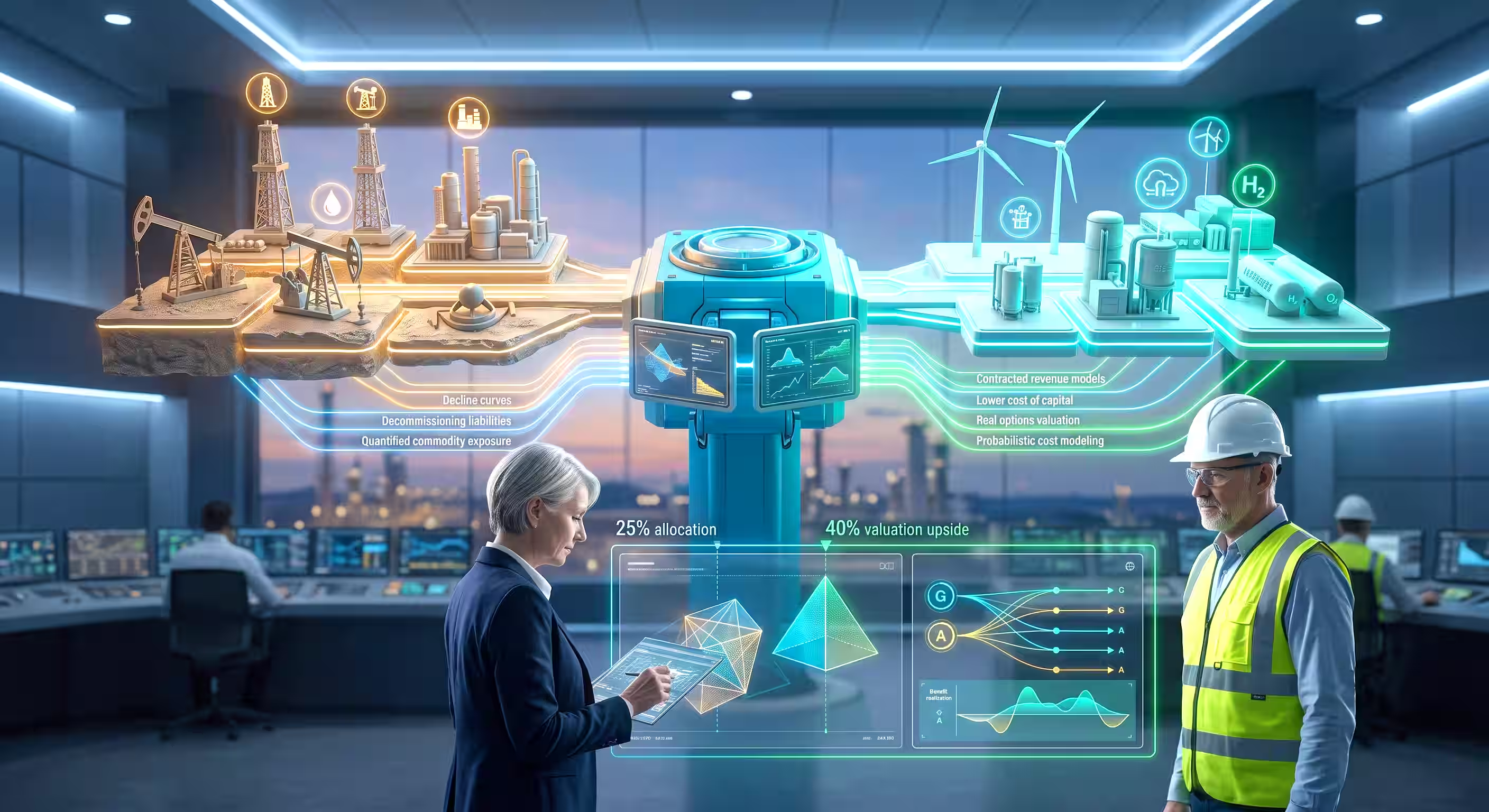

- McKinsey research indicates valuation upside starts to materialise when more than 40 per cent of a portfolio is low carbon, yet most majors allocate less than 25 per cent of new investment to new energies.

- An IPA survey found that a substantial share of renewable energy projects either bypass the gated process or follow no consistent process at all.

- Governance, not strategy, is where the dual mandate is won or lost: capital allocation, risk quantification, incentive design and assurance must work across both portfolios without forcing one set of rules onto the other.

The oil and gas industry has spent the last decade debating its strategy for the energy transition. That debate is largely settled. Most large operators now hold a position: sustain the hydrocarbon core, invest selectively in low-carbon growth, and let the pace of the transition determine the mix. What remains unsettled, and far less discussed, is how to govern the result.

The numbers describe the scale of the shift. Global energy investment reached a record USD 3.3 trillion in 2025, and clean energy technologies attracted roughly twice the capital of oil, natural gas and coal combined, according to the IEA World Energy Investment 2025 report. In the same year, upstream oil investment recorded its first year-on-year fall since the Covid slump in 2020, and roughly 40 per cent of remaining upstream spend went to maintaining production at existing fields rather than developing new ones.

For an oil and gas company, this creates what we call the dual mandate: govern a mature, cash-generating hydrocarbon portfolio through managed decline or disciplined sustainment, while simultaneously building capability in transition assets that behave nothing like the core business. Both mandates draw on the same balance sheet, the same board and, in most organisations, the same governance machinery. That is where the problems begin.

Why Does the Dual Mandate Break Conventional Portfolio Governance?

Hydrocarbon and transition assets differ in almost every variable that governance is designed to control. Return profiles, capital intensity, cycle length, offtake certainty, regulatory exposure and technology maturity all diverge. A deepwater development and an offshore wind farm may both be billion-dollar capital projects, but they are not the same asset class, and treating them as interchangeable line items in a single capital plan misprices both.

Capital markets have noticed. McKinsey's January 2026 analysis of oil and gas operating models observes that markets are increasingly sceptical of companies' ability to create value from portfolios that span diverse risk and return profiles, and notes that many companies have found organisational integration to be more of a hindrance than a help when building new energy businesses. Several majors have publicly recalibrated their transition investment as a result.

The uncomfortable middle ground is well documented. Earlier McKinsey research found that meaningful valuation upside starts to materialise when more than 40 per cent of a company's total portfolio is low carbon, while leading oil and gas majors typically allocate less than 25 per cent of new investment to new energies. Companies sitting between those thresholds carry the costs of two operating models without the valuation benefits of either. Crossing that middle ground is constrained by hard realities: the scale mismatch between hydrocarbon cash flows and typical low-carbon project sizes, and the limited supply of bankable transition opportunities offering comparable returns. Governance cannot manufacture investment-grade projects. What it determines is whether the middle ground is crossed deliberately, with clear-eyed trade-offs, or drifted through by default.

Where Does Governance Actually Fail?

In our experience across Energy, Minerals and Resources capital programmes, dual-mandate governance fails in five predictable places.

1. Capital allocation that ignores asset-class differences

Most capital allocation frameworks in oil and gas were built to rank hydrocarbon opportunities against each other: hurdle rates calibrated to commodity price decks, risking conventions built from decades of drilling data, and payback expectations set by reservoir economics. Run a wind, hydrogen or carbon capture opportunity through the same framework and it will usually lose, not because it destroys value but because the framework cannot see the value it creates: contracted revenue streams, lower cost of capital, optionality on policy support and portfolio risk reduction. The fix is not to abandon rigour but to build value frameworks that quantify return, risk and strategic fit on terms appropriate to each asset class, then make the trade-offs explicitly at portfolio level.

2. Stage gates that quietly stop applying

The front-end discipline that oil and gas built over decades does not automatically transfer to transition assets. An IPA survey of energy companies found:

- 60 per cent run renewable energy projects through a similar gated process, but those processes are sometimes expedited, still in development, or simply bypassed by management.

- 40 per cent either follow a different process or none at all.

IPA also notes that offshore and onshore wind projects are highly susceptible to cost growth and schedule slip, with risk increasingly transferring from EPC contractors to owners. In other words, the asset class least familiar to the organisation is often the one receiving the least front-end scrutiny, at exactly the moment owners are absorbing more delivery risk.

3. Risk quantification that stays qualitative on one side of the portfolio

Hydrocarbon risk is quantified habitually: subsurface uncertainty, commodity exposure and decommissioning liabilities all have established methods. Transition-asset risk tends to arrive at boards as narrative: policy support "may change", supply chains "remain tight", technology "is maturing". A dual-mandate portfolio needs both sides quantified on a comparable basis, including the interaction between them, so that Boards can see the genuine risk-adjusted position of the whole portfolio rather than a precise number for one half and an adjective for the other. The methods exist: real options valuation for policy and offtake uncertainty, scenario-weighted analysis for technology maturation, and probabilistic cost modelling drawn from the right reference class of comparable projects. Independent quantification matters here because internal teams sponsoring transition growth face an obvious incentive conflict when asked to risk their own business case.

4. M&A diligence built for one asset class applied to another

Consolidation is reshaping the sector. Wood Mackenzie recorded the seventh consecutive half-year decline in upstream deal volumes in H1 2025, even as disclosed deal value of USD 71 billion ran well above the five-year average: fewer, larger, more consequential transactions. Meanwhile transition-asset M&A continues alongside. The diligence disciplines are not interchangeable. Reserve verification, decline curves and abandonment liabilities are mature practices; assessing grid connection risk, offtake counterparty strength or hydrogen technology readiness is not something most oil and gas deal teams have done twenty times before. Portfolio transformation through acquisition demands diligence governance matched to what is actually being bought.

5. Incentive structures that pull against the strategy

The quietest failure mode sits in the scorecard. Where executive remuneration remains weighted towards reserve replacement, production growth and hydrocarbon free cash flow, governance frameworks will be outvoted by the incentives beneath them. Managers optimise what they are paid to optimise. Aligning long-term incentive plans and performance metrics with what the dual mandate actually requires, including transition-asset returns and delivery outcomes, is part of the governance design, not separate from it.

What Does Good Dual-Mandate Governance Look Like?

The organisations handling this well share three characteristics.

One portfolio, two lenses. They govern a single capital portfolio with unified strategic oversight, but apply asset-class-appropriate evaluation criteria beneath it. In practice this means dual-track hurdle guidelines, investment committees with genuine transition-asset expertise sitting alongside subsurface expertise, and value frameworks that score each opportunity against its own reference class. The Board sees one integrated picture; the machinery below it does not pretend a solar farm is an oil field. That segmentation extends within the transition portfolio itself: a carbon capture pilot should be governed for iterative learning and tolerable failure, while a scaled offshore wind development demands full capital discipline. One rigid lens applied to both misgoverns each.

Deliberate capability building. They treat transition-asset governance capability as something to be built and assured, not assumed. Concretely: gated processes designed for early-commitment assets, estimating and benchmarking data drawn from the right reference class, and owner teams staffed and trained for the risks they are actually carrying rather than the risks they know from hydrocarbons.

Independent verification across both mandates. They subject transition investments to the same independent assurance that mature capital programmes receive, precisely because internal enthusiasm for new business lines is highest where institutional experience is lowest. Independent review of business cases, front-end definition and benefit realisation closes the gap between what is reported to the Board and what is actually happening in the portfolio.

This is the thread that connects portfolio transformation to delivery. As we argued in The Gap Between Capital Strategy and Capital Delivery, a project delivered on cost and schedule can still fail if the benefit case has quietly invalidated. In a dual-mandate portfolio, that risk doubles, because the benefit cases on each side of the portfolio can invalidate for entirely different reasons.

Governing the Transition as a Portfolio, Not a Pivot

The dual mandate is not a transitional inconvenience that will resolve itself. Hydrocarbon and low-carbon assets will coexist on oil and gas balance sheets for decades, and the capital flowing to both is now measured in the trillions. The companies that create value through this period will not be the ones with the boldest transition announcements or the most defiant hydrocarbon commitments. They will be the ones whose governance can hold two asset classes to appropriately different standards inside one disciplined portfolio, and prove to their Boards and investors that both are performing.

That is a capability question as much as a capital question, and the commodity cycle will test it: the discipline built in stronger years is what stops transition capital being reflexively raided when prices fall. For a broader view of the strategic levers available, see our earlier guide to oil and gas portfolio transformation strategies, and for the questions Boards should be putting to management, see What Boards Should Be Asking About Their Capital Projects Right Now.

-----

PDAS provides independent portfolio governance, investment analysis and assurance for Energy, Minerals and Resources organisations navigating the dual mandate, from value framework design and capital allocation discipline to independent verification of transition business cases.